Anyone who has tried to buy a home over the past two years has felt the frustration: fewer listings, stalled transactions, and prices that stubbornly refuse to come down. Sales activity is weak, affordability is strained, yet home values remain elevated.

The issue is not a lack of willing buyers or even a lack of homeowners who would like to move. It is that many potential sellers are unwilling to accept that their home may be worth less than it was at the peak, and they don’t have to sell.

To understand why the market feels stuck, it helps to compare residential real estate with commercial real estate, a market that has already adjusted.

A Tale of Two Real Estate Markets

Commercial real estate repriced quickly when interest rates surged. As financing costs rose, what buyers were willing and able to pay declined. Higher rates mathematically reduced property values by pushing cap rates higher and compressing prices.

At the same time, many commercial owners faced refinancing deadlines, loan covenant pressures, or investor redemptions. These owners were forced to sell at prevailing market prices, not at valuations set during the low-rate era. Prices fell because transactions had to clear at levels consistent with higher financing costs.

Residential real estate followed a different path.

Mortgage rates also rose sharply for homeowners, but most did not face refinancing cliffs or maturity walls. They were not compelled to sell into a weaker market. As a result, listings declined, transactions slowed dramatically, and prices largely held not because demand was unaffected, but because sellers were not required to meet it.

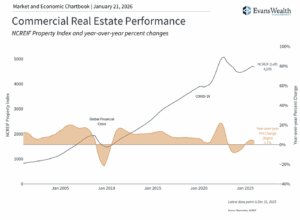

Commercial Real Estate Has Already Repriced

The adjustment in commercial real estate is clear. According to the NCREIF Property Index, which tracks private, institutional-quality commercial real estate, property values declined approximately 18.7% from their 2021 peak to their 2023 trough. This reflects higher interest rates, rising cap rates, and weakening fundamentals across several property types, particularly office. See the chart below for more.

Residential housing has avoided a similar repricing largely because homeowners are not forced sellers.

Homeowners Want to Move — Just Not at Today’s Prices

A key dynamic in today’s housing market is that many homeowners would like to move for lifestyle, family, or job reasons. But they are anchored to two things:

- The low mortgage rate on their existing home, and

- The belief that their home should still command its prior peak value.

Accepting a lower price is optional. Homeowners can wait.

This dynamic keeps inventory tight. Potential sellers stay put rather than accept a perceived loss, even if that loss is largely theoretical. The result is muted price discovery and persistently low transaction volume.

What Would Need to Happen to Energize Residential Real Estate

For the housing market to regain momentum, one of several things would need to occur.

According to Realtor.com, returning affordability to 2019 levels would require:

- A 56% increase in median household income,

- Mortgage rates are falling to around 2.65%, or

- Home prices are declining by approximately 35%.

Each path highlights the same constraint: prices remain high relative to incomes, and neither has adjusted enough to restore balance.

Lower rates, longer loan terms, or buyer incentives may help at the margin, but without a meaningful increase in housing supply, these measures risk sustaining prices rather than resolving the imbalance.

The Central Constraint

Home prices can decline only if sellers choose to accept lower valuations. Incomes can restore affordability only if wage growth outpaces home price appreciation for an extended period. Policymakers can influence incentives and financing conditions, but they cannot compel homeowners to sell or dictate market-clearing prices.

As long as most homeowners retain the ability to wait, the housing market is more likely to remain slow than corrective.

The Bottom Line

Commercial real estate has already adjusted to higher interest rates, with institutional property values down nearly 19% from peak to trough. Residential housing has not, because homeowners retain the option not to sell, and many are unwilling to accept lower prices.

Until prices decline, incomes rise meaningfully, or housing supply increases materially, the residential housing market is likely to remain slow and constrained. Stability has been preserved, but at the cost of mobility and affordability.