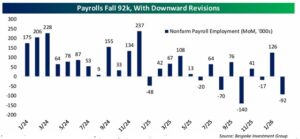

Friday’s nonfarm payroll report (3/6/2026) showed a decline of 92,000 jobs in February, well below expectations as economists had been forecasting an increase of roughly 55,000 jobs. The surprise sent the stock market down 1.33% on the day. When markets see negative job growth, especially relative to expectations, the immediate reaction is often concern that the labor market, and perhaps the broader economy, may be beginning to weaken.

But one jobs report rarely tells the full story. A closer look at the details behind February’s numbers reveals several factors that may have influenced the headline figure and could help explain why the data surprised economists.

A Strike That Distorted the Data

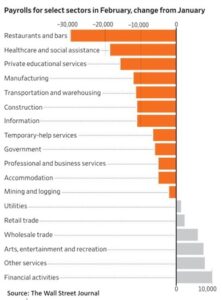

One of the biggest contributors to February’s weakness was in private payrolls, which fell by 86,000 jobs. A large portion of that decline appears to be related to a nurses’ strike at Kaiser

Permanente in California.

Because of the strike, employment at physicians’ offices dropped by 37,400 jobs. Importantly, this type of decline is typically temporary rather than structural. Once the strike ends and workers return, those jobs generally show up again in the following report or two.

In other words, this portion of the drop is likely to reverse itself in the coming months.

Payroll Data Has Been Unusually Volatile

Another important factor is the recent volatility in payroll reports.

Just one month ago, January’s payroll numbers surged sharply higher, surprising economists to the upside. It’s not uncommon for a strong month to be followed by a weaker one as the data normalizes.

There was also a negative February adjustment tied to temporary help services, which was later revised away. Temporary staffing is often one of the more volatile components of the labor market and can exaggerate month-to-month swings in the headline number.

Taken together, these factors suggest that statistical noise may be playing a larger role than underlying economic weakness.

Young Workers Are Holding Up

Another interesting data point challenges last year’s concerns that artificial intelligence would disproportionately displace younger workers. The unemployment rate for workers aged 20–24 has declined since the fourth quarter and now sits roughly where it was two years ago. Rather than showing early signs of AI-driven job losses, the data suggests younger workers are continuing to find opportunities in the current labor market.

Wage Growth Is Still Outpacing Inflation

Even if employment growth is slowing somewhat, income trends remain healthy.

Aggregate Payroll Disbursals for private non-managerial workers, a measure of the total wages paid to the largest portion of the workforce, are still growing at roughly a 4% annual rate.

That pace is higher than current inflation, meaning real incomes for many workers are still increasing. Rising real wages generally support consumer spending, which remains a key driver of economic growth.

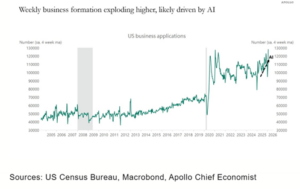

Business Formation Is Surging

Another encouraging signal comes from new business formation, which has been accelerating sharply in recent weeks.

While several factors could be contributing to this trend, it’s reasonable to believe that advances in AI and digital tools are lowering the barriers to starting new companies.

Historically, periods of strong business creation often lead to future job growth as new firms expand, hire employees, and generate additional demand throughout the economy.

One Report Doesn’t Make a Trend

Taken in isolation, February’s negative payroll print can look alarming. But once you account for strike activity, statistical volatility, and broader labor market trends, the picture becomes more nuanced.

At this stage:

- The labor market appears to be cooling, but not collapsing.

- Income growth remains solid.

- Entrepreneurial activity is rising, which could support future hiring.

For now, February’s report is best viewed as a data point worth watching, not a definitive signal of what lies ahead.