Key Takeaways:

- The AI investment boom mirrors past market cycles like the internet era, with valuations being increasingly driven by momentum.

- While AI infrastructure and semiconductor stocks have surged, software stocks have fallen 30–35% since September 2025, reflecting investor uncertainty over how AI will reshape the sector.

- The markets are experiencing intensifying concentration risk, with a small group of perceived winners absorbing an outsized share of market flows.

- History suggests cycles end not when innovation fails, but when expectations outpace reality.

The stock market has always reflected a mix of fundamentals, psychology, and speculation. But today’s market presents two unusual dynamics at the same time.

On one side, investors are aggressively chasing a narrow group of AI-related winners, particularly semiconductors and infrastructure providers, pushing valuations ever higher in what increasingly resembles speculative momentum investing. On the other side, software stocks have experienced a roughly 30% drawdown since September 2025 despite the absence of a recession, something historically uncommon for the sector.

Together, these developments represent a split reality in technology and AI related stocks, all driven by the same AI bullish thesis.

The Speculative Mentality Behind the AI Trade

Every generation experiences a dominant investment theme: railroads, the internet, housing, and now artificial intelligence.

Importantly, many of these themes were fundamentally correct. AI will likely reshape large parts of the global economy. But history repeatedly shows that a correct thesis does not always lead to a correct investment outcome if valuations become detached from reality.

Today’s AI rally is increasingly driven by concentration and momentum. Capital continues flowing into a relatively small group of perceived winners, creating a self-reinforcing cycle where rising prices attract more buyers and fear of missing out overrides valuation discipline.

That does not mean the leading AI companies are weak businesses. In many cases, they are generating enormous cash flow while investing heavily in data centers, chips, and infrastructure to support very real demand growth.

The risk for investors is not necessarily that AI fails, but that expectations and valuation multiples may already assume years of near-perfect execution.

The Software Reset

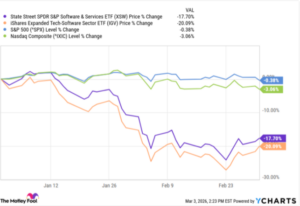

While AI infrastructure stocks have surged, software companies have moved sharply in the opposite direction. See the chart below.

The S&P North American Technology Software Index has fallen roughly 30–35% from its September 2025 peak despite no traditional recession or financial crisis. Historically, this type of software correction typically required a broader economic downturn.

This time, however, the weakness appears tied less to economic weakness or overvaluation and more to uncertainty surrounding how AI may reshape the software industry itself. Investors are reassessing each software firm’s future growth expectations and ability to defend their turf against rapidly evolving competitors.

Maybe investor fears ultimately prove justified. Maybe they do not. But the uncertainty has been enough to trigger a meaningful repricing across the sector.

At the same time, the dynamic reinforces the broader market enthusiasm surrounding AI. Capital has increasingly flowed out of software and into AI infrastructure and semiconductor companies, intensifying the concentration in perceived AI winners.

What Investors Should Take Away

That does not mean the AI thesis is wrong. AI will likely prove transformative over time. But investing success depends not only on identifying powerful long-term trends. It also depends on the price paid for exposure to those trends.

History repeatedly shows that even revolutionary technologies can produce disappointing investment returns when expectations move too far ahead of fundamentals.

Markets repeatedly cycle between optimism and discipline. During euphoric periods, investors convince themselves that “this time is different.” Eventually, fundamentals reassert themselves.

The current environment may ultimately be remembered as both a period of extraordinary AI-driven innovation and a reminder that valuation still matters.

Cycles rarely end because innovation fails. They end because expectations become unsustainably high.